The Quest for Low-Risk Loans

Lending companies are only able to make a profit if their clients pay back their loans. But how do you know which client to lend to? And how much to lend? These are the type of questions that can make or break a financing firm, and that’s why Business Backer, a lending firm for small businesses, decided to tackle these questions head-on. While the company has had considerable success—they have secured $130 million in funding to more than 4,000 small businesses across the United States--they wanted to take guesswork out of the equation.

To answer their questions, they turned to Albert Fensterstock, Managing Director at Albert Fensterstock Associates, who specializes in improving risk analysis capability and collection department efficiency. Fensterstock, in turn, relied on Palisade’s NeuralTools software to help Business Backer begin refining their decision-making process. “I’ve used Palisade’s products for years,” says Fensterstock. “And I used it this time to answer a two-fold problem: How to make a loan with less risk, and how to come up with an appropriate credit limit.”

Prior to putting Palisade’s software to work, Business Backer’s analysts relied on subjective techniques to review potential debtors. This meant the analysts selected factors and weighted them according to their perceived level of importance. However, this technique was flawed. “If you took ten credit managers and asked them to come up with a list of factors, each one would have a different set. Alternatively, if you gave them the factors, they would each weigh them differently,” Fensterstock explains.

Applying the Brain Power of NeuralTools to Historical Data

Instead, he applied a more scientific approach to determine which factors were important in choosing a potential client. Variables could include data such as credit balance, late fees, the size of a company, number of years in business, credit limit, and net worth, to name a few. Using thousands of historical accounts from the Business Backer database, Fensterstock created over a hundred models with NeuralTools to see which factors were actually predictive of a client being reliable with their payments. NeuralTools, as sophisticated neural networks software, is capable of learning complex relationships in data. Specifically, by mimicking the functions of the brain, it can discern patterns in data, and then extrapolate predictions when given new data.

From running these models in NeuralTools, Fensterstock could pick out which variables related to the potential debtors were useful, and which weren’t. Here, NeuralTools provided a Variable Impact Analysis that measures the sensitivity of predictions to changes in the independent variables and lets the analyst know how much each variable affects the predictions. This, plus other tests conducted with the help of Palisade’s statistics toolkit StatTools, allowed Fensterstock to choose the most predictive variables from over 100 that were initially available.

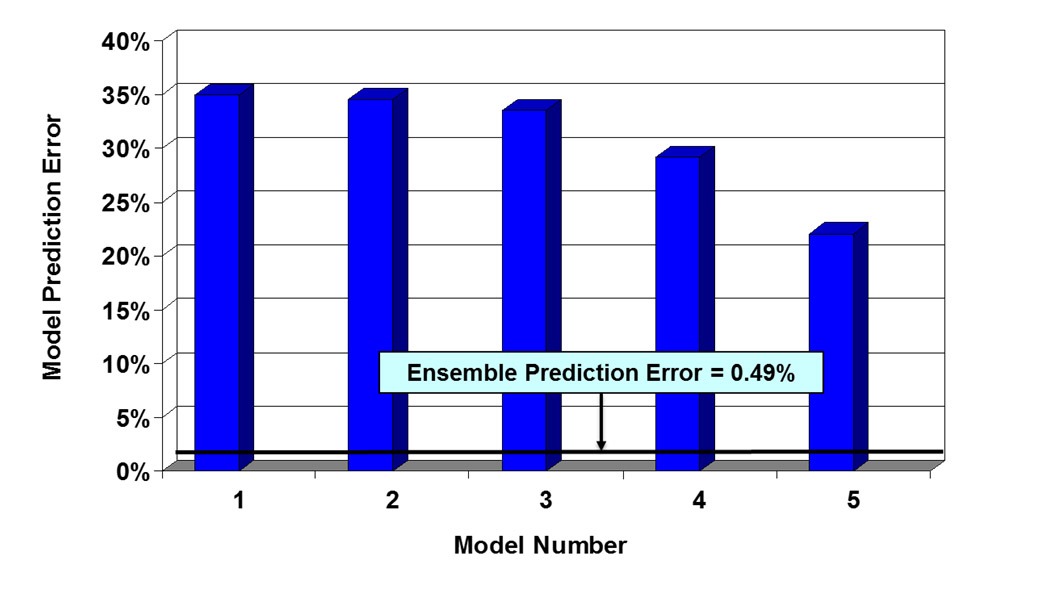

With the right factors in hand, Fensterstock built an initial kitchen sink model that used 25 key variables proven predictive in his previous screening process. When Fensterstock ran the historical data through this single sparse model, it was not any better at predicting who would default on their loans than the earlier, subjective technique used by Business Backer, and had a prediction error rate that was unacceptable.

Strength in Numbers

To combat this error rate, Fensterstock decided to create what’s known as an ensemble model. Ensembles combine multiple models, or hypotheses to form a better hypothesis. Therefore, an ensemble is a technique for combining diverse models in an attempt to produce one that is stronger than any individual model. By combining five different neural models within NeuralTools and weighting their output, Fensterstock was able to get the ensemble model’s prediction error rate down to just under 0.5%. “At that point, we had a good predictor of who is going to pay their loans back,” says Fensterstock. “The next step was then to figure out how much to loan them.”

Albert Fensterstock

Lend some Flexibility

A common mistake made by financing firms, Fensterstock says, is to only evaluate a client based on the amount they ask to borrow. For example, a small business wants to borrow $50,000, but the ensemble model determines that they would default. Even so, the small business may still be a viable client for borrowing $30,000. However, many lending firms do not apply this extra level of consideration, thus turning away extra business.

Conversely, if the ensemble model test initially approves a potential client to borrow $50,000, “Why not run the model with that client for a $60,000 loan?” says Fensterstock. “We can raise that loan amount until the model doesn’t like him, essentially establishing a credit limit and offer them a higher amount, thereby increasing Business Backer’s profit margin.”

Chasing the Right Target

After creating these more nuanced models for Business Backer, Fensterstock then turned to fine-tuning the collection process of the business. He designed the system so that the clients’ portfolios are rescored every month to ensure that their current implied risk of default is not significantly greater than it was at the time the loan was granted. “We were able to get ongoing bank data from these clients as part of the loan term,” says Fensterstock. “That way, if a business owner’s circumstances have changed, we would have an early warning system in place, and the collectors can get first in line to get paid.”

Finally, Fensterstock created an analytics system with NeuralTools that predicted how likely a debtor was to pay back the loan. “There are different kinds of accounts,” he says. “Some you will never get a nickel from, while others you will have a good chance of collecting the money.”

Fensterstock further explains that lending firms that don’t use a model-based approach will simply go after the debtor who owes them the most money for the longest amount of time. With the help of a model, a lender can take a smarter approach: “Perhaps you have a debtor who owes you $50,000 but only has a 5% chance of ever paying it back, whereas there may be someone who owes you $5,000 but has an 80% chance of paying it back. Knowing those chances of repayment can help lenders know which debtor is worth going after for repayment,” says Fensterstock.

Overall, the models Fensterstock developed for Business Backer set an impressive precedent. “I’ve been doing this kind of work for 22 years, and I’ve never before built models that were able to do this in one task,” he says. “This model is better than anything I’ve ever developed.”

Fensterstock says that NeuralTools made the work all the easier thanks to its ease of use and its seamless integration with Excel. “Basically, the Palisade tools are great to work with.”