Background

The UK government’s Department of Energy and Climate Change (DECC), is tasked with maintaining secure and economic energy supplies for the UK, while ensuring that the UK’s greenhouse gas emissions meet international targets set to combat climate change.

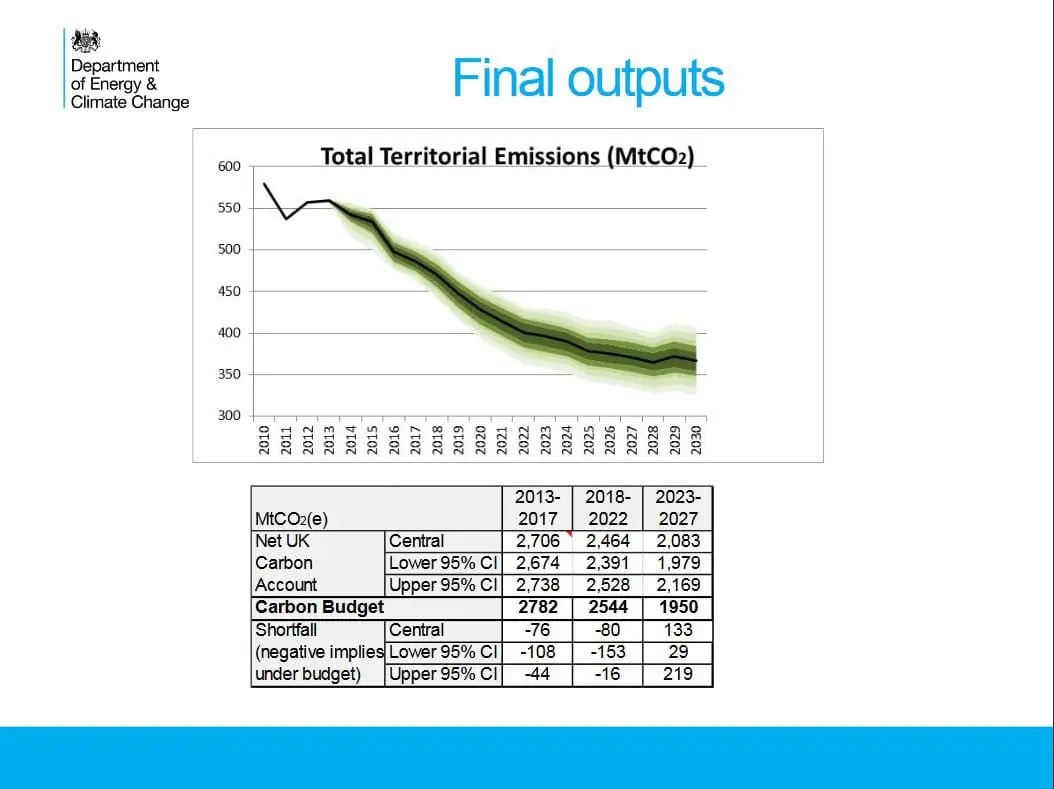

Under the Climate Change Act, the UK has a legal obligation to meet several national emission targets, called carbon budgets, including cutting UK greenhouse gas emissions by at least 80% by 2050 (which requires sourcing at least 15% of energy from renewable sources by 2020).

To monitor carbon budgets, the Central Modelling Team at the DECC undertakes annual projections of energy use and emissions by modelling both overall UK energy demand and the electricity supply system and calculating the emissions based on the fuels used. These projection figures are uncertain however, due to variation in each of the economic and technical inputs used in the models. DECC uses @RISK to explore the overall effects of these uncertainties and estimate the probabilities of not meeting the carbon budget.

Using @RISK to assess overall impact of different inputs

The DECC Central Modelling Team works with a huge range of inputs. These include government policies and macroscopic variables such as GDP and population that have an effect across many economic sectors. In addition there are more specific inputs such as fuel prices (which determine how much fuel is used, both in vehicles and elsewhere), vehicle efficiencies and the number of ‘winter degree days’ (a measure of the length of periods of cold weather).

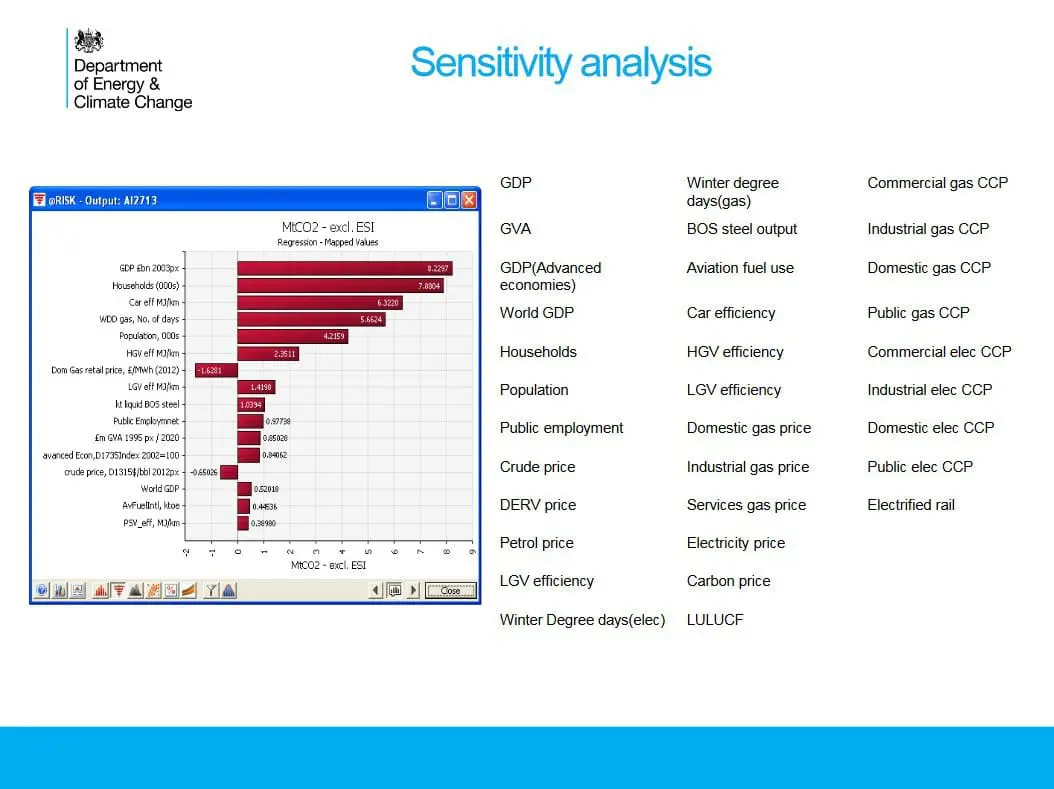

Using @RISK to create a Tornado diagram, the Central Modelling Team assesses how sensitive overall emissions are to changes in the values of selected input variables. This allows it to restrict the final Monte Carlo analysis to the variables that have the most impact on the UK’s emissions.

The government has an extensive history of collecting economic and other statistics and this allows robust analysis of the data. GDP data is available going back to 1970 and @RISK can be used to calculate the statistical distribution of year-on-year economic growth. Similar procedures for the other key variables result in around 20 distributions to use in the modelling. For each year of interest, a value can be sampled from each distribution and these values inserted into the emissions projection model. After 1000 or so iterations, a distribution can be created at each year and the uncertainty estimated.

Dr. Roger Lampert

ECC Central Modelling Team

@RISK imposes rigour and accountability on modelling results

“@RISK has all the sophisticated functionality required for Monte Carlo modelling, but is straightforward to use,” explains Dr Roger Lampert from the DECC Central Modelling Team. “Before adopting Monte Carlo modelling, the custom was to use scenario analysis. Using @RISK we can now use the statistical properties of the input data to better represent the full spectrum of possible model inputs. Consequently, we have more insight into the spectrum of outputs. The statistical rigour of the modelling gives us much more confidence in the level of uncertainty of our emissions estimates and therefore the UK’s ability to meet the carbon budgets.”

Most useful software features

@RISK’s distribution fitting functionality: Its different fitting criteria and its ability to easily see the proportions of distributions that are around a particular value allows the DECC modelling team to determine which of the acceptable distributions are the best fit for the data.

In addition, sensitivity analysis with Tornado diagrams is an efficient way to filter the model inputs to discover those that have the most impact on the results, thereby saving time and resource. Many of these significant variables exhibit both autocorrelation and cross-correlation and hence tend to move in the same way. For example, GDP and Gross Value Added are closely related and it would be extraordinary if one increased by a large amount whilst the other decreased, but this can happen in a model where they are treated independently. @RISK makes it easy to account for this in the modelling by explicitly defining a correlation between different variables and even the same variable over many time periods.

Specific techniques

The Central Modelling team at DECC uses Time Series Econometrics to derive many of the equations in its models. A particular property of Time Series is their ‘stationarity’ and this must be accounted for in order to avoid a false illusion of correlation between variables. Recent upgrades of @RISK now include a test for stationarity so this can now be done within the analysis, which simplifies the work.

Distributions used

@RISK is particularly good at distribution fitting and the DECC uses a wide range of distributions, including Laplace, Triangular, Exponential and Uniform. It is frequently found that there are several distributions that have an acceptable fit to the data and it may be possible to choose a ‘best fit’ using different criteria. A particular example is GDP, where @RISK aids in selecting a fit that best represents the frequency of recessions as well as having an acceptable fitting parameter. The graphical output of the distributions makes it easy to see the years when growth was negative.